Article | Feb 2021

The Return of the Executive Mega Grant: Are They Really Worth It?

There are multiple factors to weigh when deciding if a “mega grant” is the right compensation strategy for your business circumstances.

Several recent inquiries from clients in high-growth industries point to a potential comeback for the “mega grant.” Mega grants are not a new concept—they were popular in the early 2010s before fading somewhat, likely due to pressure from shareholder advisory groups that prefer more traditional annual equity grant programs. Today, they seem poised for a comeback.

What makes a mega grant? There’s no set definition, but generally it’s an award that exhibits at least some of the following characteristics:

- A grant date value of more than 10x the CEO’s (or other executive’s) salary;

- Represents a significant percent of common shares outstanding (e.g., 3% to 12% or more of common stock outstanding [CSO]);

- A one-time multi-year award, with an expectation of no further equity awards being provided to the recipient for several years; and/or

- Extended vesting/performance horizons, often seven to 10 years.

Perhaps the most well-known recent mega grant was made to Tesla founder Elon Musk in 2018. With a whopping grant-date value of almost $2.3 billion, the performance-based option award to purchase 20 million shares (on a pre-split basis) would transfer up to 12% of common shares outstanding at the time over a period of up to 10 years. The award was ultimately split into 12 equal tranches, each of which provide an extra point of equity as market cap and operating performance milestones are attained. With Tesla’s recent strong share price performance, revenue growth and EBITDA growth, four of 12 tranches have now vested, with a current value of approximately $28 billion.

Looking at the Tesla case, mega grants may seem like an effective incentive tool. It’s hard to imagine an award structure that more closely aligns executive and shareholder interests, and as such, there may be unique circumstances where time, place, and personality type converge to make such a structure work well. However, before making or requesting a mega grant of your own, consider the following factors during the decision-making process.

Pay for Performance

Assuming proper goal-setting, it’s hard to think of a better way to link pay and performance than with a performance-based mega grant. With appropriate goals in place, it positions executives to put their money where their mouth is. With a mega grant, they are betting on themselves, their colleagues, and the business to deliver results that drive value. It’s possible, however, that the pay-for-performance sensitivity is almost too high—vesting triggers are often binary leading to “all or nothing” scenarios that are hard to unwind (more on this below).

Dilution

Undoubtedly this will be the first thing that comes to your investors’ minds when you say the words mega grant, and who can blame them? Mega grants are potentially very dilutive to shareholders, and prudent investors will always be focused on how equity compensation can reduce the relative weight of their own stakes over time. While dilution is rightfully a concern, it can be a fairly straightforward trade-off with the significant value created if the performance goals are satisfied. After all, it’s much better to own a small percentage of a really big thing than a big percentage of next to nothing.

Design

Any number of bells and whistles can be attached to mega grants, though most vesting triggers are either market-related (e.g., share price growth or market cap goals), or combine market factors with other strategic or financial goals. In our experience, market performance conditions are best for mega grants given how tangible and objective they are and how efficient the stock market is at pricing in progress. Assuming reasonable checks and balances are established in the design process (i.e., a trailing average share price or market cap is used in the vesting trigger), market conditions are usually preferable over financial conditions given how difficult it is to project performance over a greater than three-year period in high-growth companies. Financial goals therefore bring a level of risk and uncertainty that we think is best to avoid.

Longevity

The time horizon for normal annual equity awards is generally thought to be three or four years. Over this period, most options, RSUs, and performance-based RSU awards vest. However, for mega grants, the time horizon is often much longer, at around seven to 10 years. This makes sense since the performance goals must be suitably aggressive to generate the value sought, which simply takes time. While most executives will understand this, it can be hard to keep the faith in years five, six, or seven of a mega grant when none of the award has vested thus far and the vesting goal still seems far away.

Adjustments

There is an old adage about best laid plans. Too often companies make mega grants to CEOs or founders only to cancel and reissue new awards some years later. If vesting becomes unlikely and the mega grant loses its relevance, the company really is between a rock and hard place. Even if the parties agree to cancel and replace, some or all of the original accounting expense must often still be recognized in addition to the accounting expense for the replacement award. But perhaps more importantly, the concept of cancel and replace goes against the very ethos of performance-based equity. If cancel and replace becomes a genuine alternative, the mega grant was in retrospect a “free option” on the future—clearly not how pay for performance is supposed to work.

Advisory Groups

Private companies pursuing a transaction or those that have recently completed one are prime candidates for considering mega grants. They are generally free from close scrutiny by ISS or Glass Lewis for at least a few years (some limited exceptions apply). Our understanding is that ISS and Glass Lewis are not philosophically opposed to mega grants; however, any post-grant modification or make-up award provided would certainly be viewed very unfavorably. It’s also worth considering how ISS or Glass Lewis might incorporate the grant date value of the award into their own pay-for-performance alignment assessments. If it’s significantly above market—and it almost certainly will be—prepare to defend the rationale in the proxy, to investors, and even to ISS and Glass Lewis to reduce the likelihood of an “Against” say-on-pay recommendation/vote.

In Summary

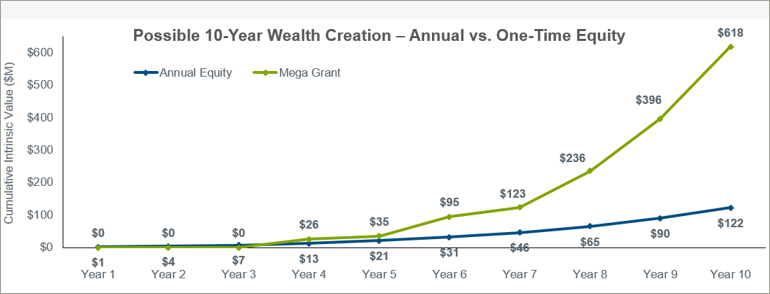

Are mega grants worth it? Maybe. In analyzing the risk/reward setup for a Tesla-style mega grant versus ongoing annual equity awards, while the potential value of a mega grant far outweighs that of annual grants, the average expected payout is likely similar when adjusted for risk. In other words, if mega grant goals are suitably aggressive, it would be reasonable to ascribe a 10% probability of achieving all of them through the life of the award. Using the example below, which assumes a potential mega grant value of $618 million, the expected value of that award is probably closer to $61.8 million (i.e., $618 million x 10% probability = $61.8 million). When compared to annual equity awards, which might comprise time-vested options, RSUs, and/or performance-vested RSUs, the potential value is lower—in this case $122 million—but there’s a much higher probability of vesting. Assuming a 50% probability, the expected value of the award is approximately $61 million, which is about the same as the mega grant.

*Assumes a 5% mega grant and Tesla’s market cap growth goals for a fictional $2B company

A time and place for mega grants certainly exists, but it’s critical to enter into these arrangements with eyes wide open and a very clear understanding by all parties of the risks for executives and shareholders. The potential for second chances should not factor into the deliberations. As with many choices in compensation, this decision comes down to good business judgment, a strong pay philosophy, and insight into what truly motivates the personalities involved. If the stars align on these three things, then a mega grant just might work.