Article | Feb 2020

The 2020 Compensation Committee Agenda: Five Pressing Issues in Focus

The emerging compensation-related trends that warrant review this year.

With the arrival of another roaring ‘20s, it’s time for boards to look ahead and prepare for the significant changes coming in corporate governance. This is particularly true for the compensation committee, whose role is expanding, while the focus on executive and director pay is increasing. We have identified five growing topics of focus that warrant the compensation committee’s attention this year.

- What exactly should directors be doing in response to the compensation committee’s expanding charter and responsibility?

- What best practices should be considered in the use of “adjusted” performance metrics for incentive programs?

- Should the compensation committee consider moving beyond disclosure to inclusion of ESG metrics in an incentive plan?

- Is it time, again, to consider EVA?

- How do we balance the pressure to be more transparent on compensation matters with the risks of sharing too much information?

1. Expanded Responsibility for the Compensation Committee

The role of the compensation committee has continued to expand to incorporate responsibility for a broader range of human capital issues including succession planning, leadership development, corporate culture, and diversity and inclusion. In general, we are seeing an increasing level of focus by the board on people matters that reach beyond the C-suite.

This starts with leadership selection and talent development programs but has of necessity evolved to risk management—dealing with investor and public confidence issues such as MeToo incidents, poor customer service, and retention issues. Most importantly, it has led to how to develop and maintain a culture that does not encourage those things to occur.

External pressures to make more rapid progress on societal issues such as diversity and pay gap come back to the board as well. (And where better to send those challenges than the compensation committee?) While there has been much conversation about these topics, what exactly should directors be doing in response to the expanding charter and responsibility?

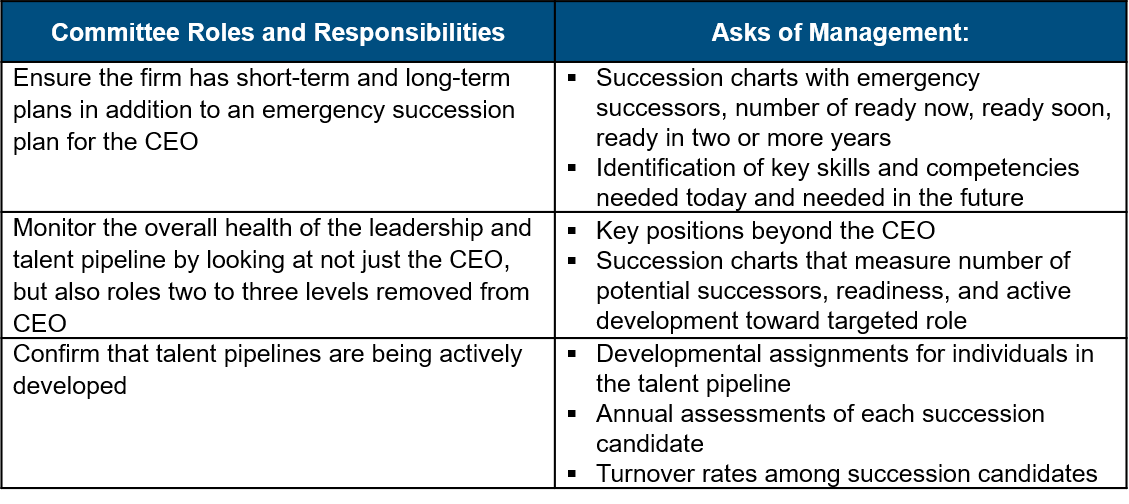

Succession Planning

While boards have typically reviewed top level succession candidates once per year, today many companies are reviewing management development programs deeper in the organization to make sure there is a robust pipeline. Specific roles and responsibilities include:

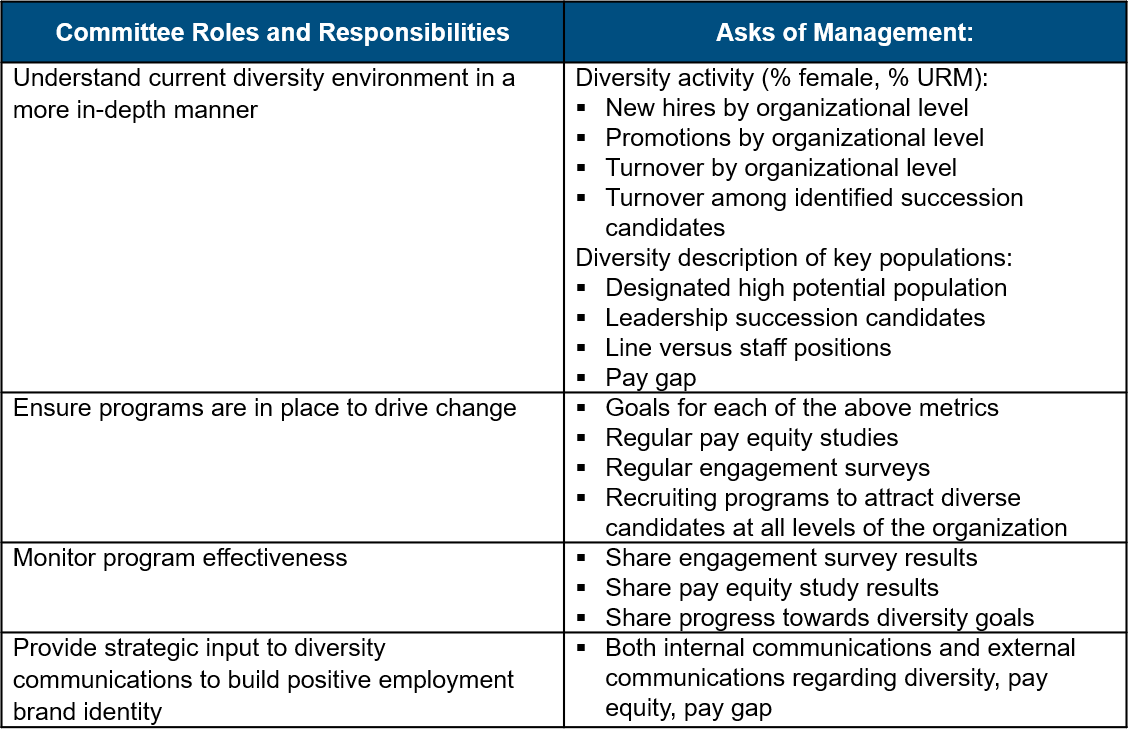

Diversity and Inclusion

While many boards have a once-a-year presentation on diversity statistics, boards are increasing their oversight of the strategies employed to make progress on diversity issues.

Expanding the role of the board and the compensation committee in broader talent management issues has been trending upward for several years and continues to gain attention as talent issues surface and potentially become the barriers to success for organizations. Continuing to recognize the human capital strategy linkage to overall success and being proactive in surfacing, discussing, and recommending action will enhance board effectiveness in delivering shareholder value.

2. Best Practices in the Use of Adjusted Performance Metrics

The vast majority of US publicly-traded companies measure and publicly communicate financial results using “adjusted” metrics in addition to the required GAAP metrics. As the term implies, adjusted performance is based on adjustments to GAAP financial results. For example, one such common metric is adjusted earnings per share.

The rationale for using adjusted metrics is to provide investors with a clearer picture of true operating performance without the distortions of one-time events such as acquisitions, divestitures, changes in accounting rules, restructurings, and legal settlements, which can result in significant year-over-year volatility in published results that may not be reflective of core operating performance.

Consistent with the approach used for financial performance disclosures, most companies also use adjusted metrics as the basis for incentive compensation payouts. In addition to maintaining alignment with how companies communicate results to investors, the rationale for using adjusted performance for incentive compensation is to motivate and reward management for delivering operating results within their control and influence.

The use of “adjusted” financial performance metrics has come under criticism from the public and scrutiny from the SEC. Critics point out that “one-time” loses its veracity when adjustments are made every year. They also note that the types of adjustments vary across companies, making relative performance comparisons difficult if not impossible.

Given this criticism that adjustments to financial metrics lack consistency across companies, what factors should compensation committees consider in allowing for adjustments to performance metrics for incentive compensation purposes?

We suggest that compensation committees consider the following “rules of the road”:

- Materiality: Consider a threshold dollar amount over which adjustments would be considered.

- Consistency: Review against historical adjustment decisions to avoid the slippery slope of new adjustments every year.

- Accountability: Evaluate the degree to which the item or event is truly outside of management’s control and not a result of core operating performance.

- Disclosure: Ensure any adjustment will withstand the bright light test of public scrutiny. Is the proposed adjustment also reported externally to investors? If not, does approving this adjustment create additional proxy disclosure burden?

While private companies may not have the same disclosure concerns, the other criteria for considering GAAP adjustments (materiality, consistency, and accountability) are just as relevant as for private company incentive plans as they are for public companies.

We also recommend that committees adopt a regular cadence of reviewing potential adjustments on a quarterly basis to avoid any unanticipated year-end surprises. In addition, committees should ask to see competitive practices as to how peer companies treat adjustments for incentive compensation purposes.

3. Is it Time for ESG to Factor in Compensation?

In 2020, addressing sustainability is not optional. Stockholders (and employees and customers) are demanding that boards be clear about companies’ positions on environmental, social, and governance (ESG) issues and more importantly, what they are doing to effect change. What does that mean in the context of executive compensation?

ESG issues, given their depth and breadth in scope, are fundamentally issues that touch all board committees. However, compensation committees are on the hook to determine if and how senior management teams should be held accountable—through their incentive plans—for achieving goals that create shareholder value while driving safe operations, turning a profit, and thriving responsibly.

These are not easy discussions to have or decisions to make. If we step back from the plethora of issues, and approach ESG more holistically, we see that it goes far beyond tactical challenges, quantifiable metrics, and checklists. The questions to tackle are complex. For example, how does an organization prioritize social issues versus its carbon footprint or how do you decide if an issue is important enough to measure, is it also important enough to pay for? The point is, deciding what goes into an incentive plan will be the result of debate and compromise and balancing the many competing priorities that are unique to your business and its stakeholders.

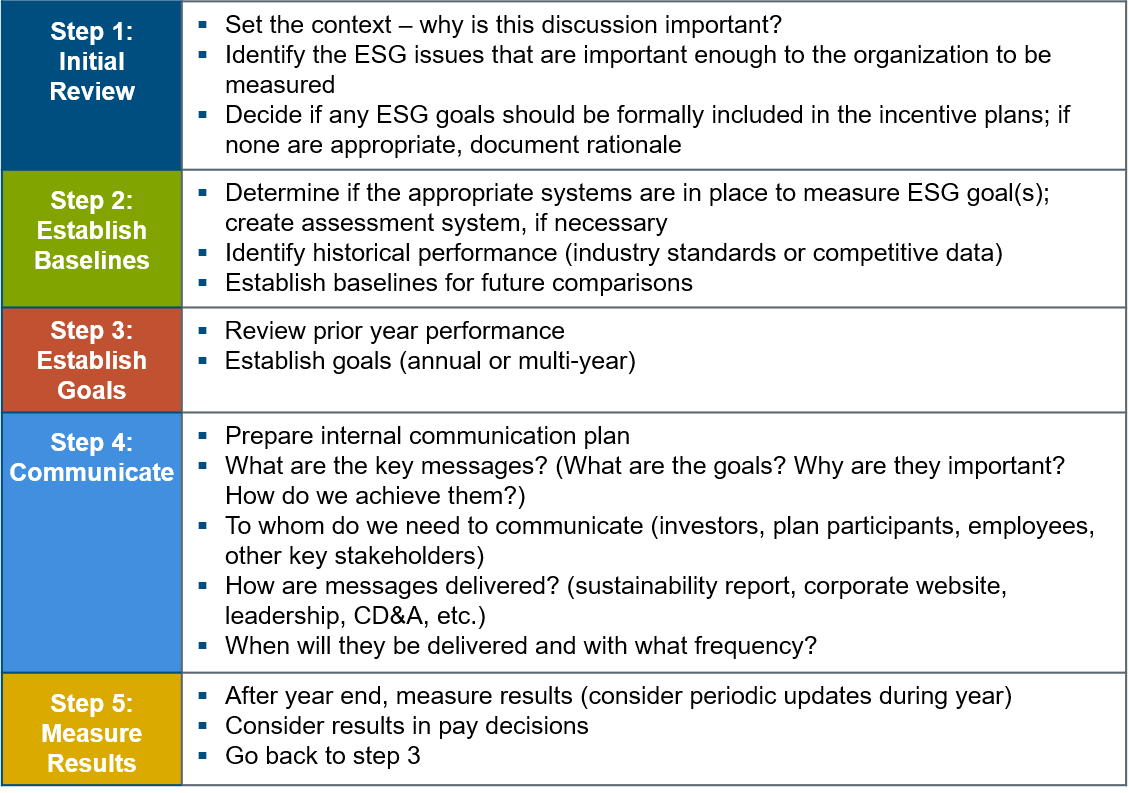

The following steps offer a basic starting point to help compensation committees begin discussions and develop a process to identify, measure, and potentially pay for driving ESG performance.

Ultimately, how a company addresses its ESG issues, including its decisions about how ESG performance measures formally or informally play a role in incentive plan payout opportunities, will be unique. Yet all companies can expect that soon enough, investors will want to know what your company has decided to do and why.

4. EVA as an Incentive Metric?

For 2020, ISS (Institutional Shareholders Services) has fully incorporated Economic Value Added (EVA) into its assessment of executive compensation. A slate of four EVA-based measures replaces the GAAP measures in the secondary Financial Performance Analysis (FPA) portion of the pay-for-performance (PFP) test.

The hard truth is that EVA is somewhat more complicated, and much less prevalent, in incentive plans than GAAP measures. Moreover, the four EVA-based metrics used by ISS may seem even further derivative and removed. Yet, it is important that your company understand these EVA measures, have an idea how it will compare in your FPA test, and have a practical and clearly communicated position regarding the use of EVA.

ISS’ EVA Measures

While the measures may be unfamiliar, there is logic and rationale to the use of the four EVA-based measures. First, EVA by itself is useful in that it captures growth, profitability, and risk-adjusted capital returns in a way no single GAAP measure can do. In order to allow for comparisons across companies of different size, EVA can be scaled, and that is what the four ISS measures do. They are size-adjusted, based on sales or invested capital. Two of the measures gauge economic profitability: “EVA margin” is the ratio of EVA to revenue, while “EVA spread” is the difference between ROIC and the cost of capital, both over a given period of time. The other two measures are both related to “EVA momentum,” which seeks to capture the change in EVA from the prior to current period, scaled by both revenue and capital.

Understanding How Your Company Will Compare

As with the GAAP measures, ISS will determine your company’s quartile performance vis-a-vis each of the four EVA measures. Your company should begin modeling the EVA measures against peers, similar to the way it models relative TSR and the legacy GAAP measures. However, ISS EVA is not a simple calculation. In fact, it is subject to fifteen standardized adjustments, from capitalization of R&D and advertising expenses to smoothing of taxes. Early reverse engineering modeling is getting reasonably close, and only a handful of the fifteen adjustments appear significant. Nevertheless, as 2020 progresses and more company reports are reviewed, modeling should improve markedly.

Is EVA Right for Your Company?

EVA has been around since at least the 1980s, enjoying a bit of a golden age in the 1990s as hundreds of publicly traded companies tried it on for size as a planning tool and/or in their incentive compensation plans. Today fewer than ten percent of US public companies use EVA (or more generically, economic profit) in their incentive plans. All of the traditional reasons for considering EVA, and for dismissing EVA, remain unchanged since ISS adopted its usage. In other words, companies should place no weight on ISS when considering EVA, or any other performance measure for incentive compensation. It is important to note that companies can include all performance dimensions of EVA in their incentive plans through a combination of measures related to growth, profitability, and capital efficiency, along with thoughtful plan design, weighting, and goal-setting. EVA is not necessary. However, the performance dimensions of EVA—profit, growth, capital efficiency—ought to be represented and properly balanced in your incentive framework and reflect your company’s specific economic context.

5. Strategic Transparency in Communicating Pay Issues

Compensation committees are recognizing that investors and proxy advisors are not the only stakeholders who need to have comfort and confidence that compensation programs are designed to be responsible, competitive, and aligned with long-term value creation. However, as the landscape of stakeholders interested in executive compensation is growing, it should be noted that they are not created equal—some carry more risk and require focused attention and/or messages. For example, investors and proxy advisory firms want companies to demonstrate robust shareholder engagement efforts and board responsiveness following a low say-on-pay result. On the other hand, high-performing employees are likely to be focused on career growth and pay equity policies. While certain consumer constituencies may be focused on environmental sustainability efforts. Companies that can clearly communicate their compensation philosophies and positions on various pay-related issues will find themselves in a better position overall with their various constituencies.

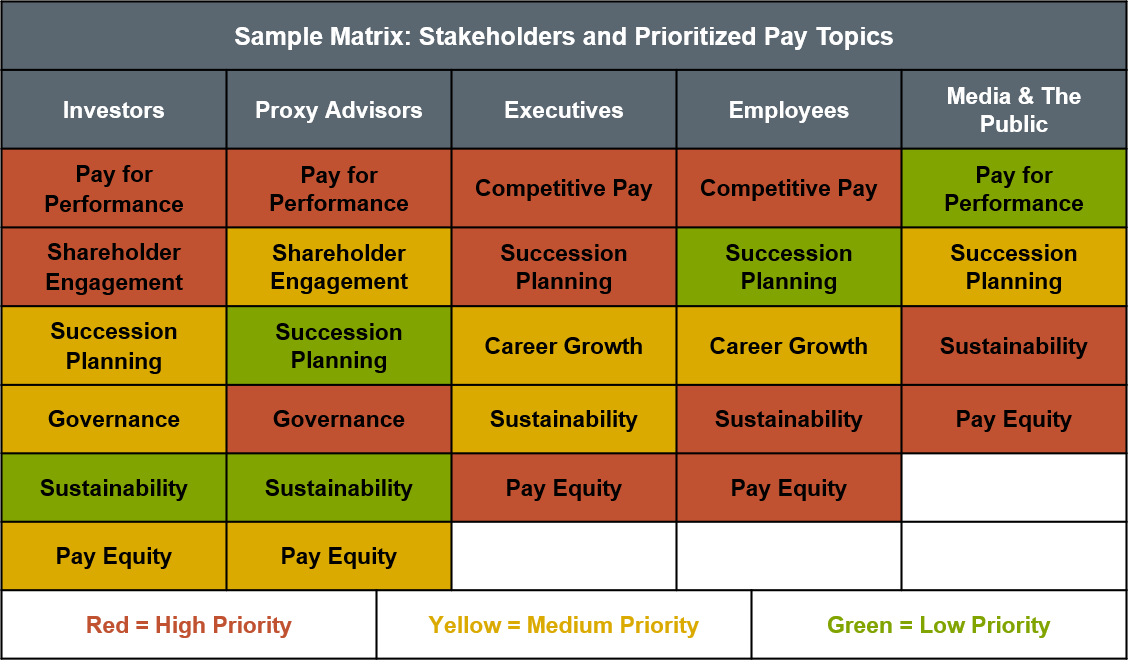

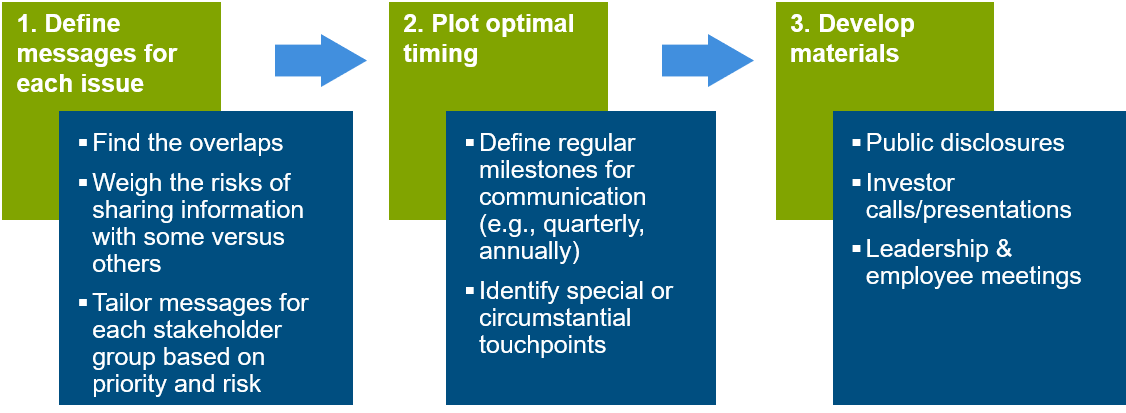

Because expectations about information vary across audience segments and some issues will be more important for some than others, the board and senior management should have a shared vision of their organization’s strategic transparency goals. The first step in ensuring that your organization is addressing the issues thoughtfully and strategically is to create a pay topic inventory list, cross-referenced with your list of stakeholders and prioritized according to audience.

After this exercise, you can begin to develop the message platform for building a “strategic transparency roadmap” with specific messages, timing, and materials. In some instances, messages will overlap which is a good thing, as continuity is critical to building credibility and ongoing trust. However, not all messages are one size, even if they are centered around the same topic. For example, your executives and employees are probably all interested in competitive pay practices. It’s probably a high priority to make sure that your employees—regardless of level—understand how the company sets pay levels and makes compensation decisions on an ongoing basis. So, your company may decide to be transparent about which and how peer companies are analyzed when benchmarking pay levels. However, executives may want more details around equity and shareholder value creation than employees who are only eligible for cash incentives.

There is no doubt that the topic of pay transparency and what it means will continue to be in the spotlight, especially as we head into the 2020 presidential election. With a clear and shared vision of what your organization wants to say about compensation to whom and when, companies will have a much better chance of mitigating any unintended consequences of staying silent on the pay issues that have become part of today’s global conversations.

Key Takeaways

Trends are by definition a general direction. As such, they warrant our careful attention and companies of all sizes and ownership structures should take note.

When it comes to the expansion of the compensation committee’s responsibilities, it’s doubtful that any company can determine “it’s not right for us.” Taking a closer look and becoming more actively involved in broad human capital issues such as succession planning, leadership development, and diversity and inclusion are becoming a key underpinning to the execution of your business strategy.

Getting performance measurement “right” continues to be a key priority for the committee—as illustrated by the fact that three of our top five topics are variations on this theme. When thoughtfully applied, “adjusted” GAAP metrics can strengthen the link between management performance and pay, but we advise companies to conduct regular reviews and develop a set of rules to guide any adjustments to ensure they are even-handed and defensible.

Similarly, companies should pay close attention to the growing call for ESG measures—this movement cannot be overlooked. Focus first on understanding your company’s baseline position, determine what matters most to your business and your constituencies, and establish broad goals. For some companies, it will be a natural next step to include one or more of those goals in executive incentive plans, while for others a strong communication plan may be the right approach.

Third, we believe that most companies, after evaluating the re-emergence of EVA, will agree that its performance dimensions—profit, growth, and capital efficiency—ought to be captured in some way in the incentive plan framework, though EVA itself may not be necessary other than as a sanity check vis-a-vis proxy advisor pay-for-performance assessments. And of course, any and all measures should reflect your unique market, operating environment, and strategy.

Lastly, there is an ever-increasing expectation on the part of all stakeholders for greater levels of communication and transparency about compensation and human capital management. We believe it is important to create a communications approach based on “strategic transparency” that targets the right audiences with the right messages. Thoughtful and consistent messaging not only prevents problems but can also improve culture and positively differentiate your organization.